Thursday, November 13, 2008

So Was Oil in a Speculative Bubble or Not?!

Over the last year, I pretty definitively painted myself into a corner regarding speculators and oil prices. I said in many places (here and here, for example) that speculators weren't driving the record run-up in oil prices, and that the default explanation--changes in the fundamentals of supply and demand--were responsible. Specifically, I testified to the committee of my good friend Barney Frank (though he actually was never in the room when I was speaking) that record oil prices were the result of a weak dollar and explosive growth in demand in places like China and India.

Well, here's a chart of oil prices:

I think we can all agree, that looks pretty bubblicious.

So what gives? Well, the thing is, I still don't see any obvious mistakes in the chain of reasoning I used in the two articles linked above. And for the record, I didn't come to the analysis thinking, "OK, for political reasons it can't be the fault of hedge funds, so I have to work some Murphy Magic here and spin a story."

On the contrary, I initially thought it was speculators in the futures market driving up oil prices, especially since the take-off in commodities really kicked in when the Fed started cutting rates in September 07. (For example, the yr/yr change in monthly oil prices was actually negative until then, but afterward of course oil prices started exploding.) So I was coming to the analysis thinking speculators were holding prices up above the equilibrium price as determined by the "short-run fundamentals" (if you will), and I was prepared to explain why that was a good thing. E.g. if the US started bombing Iran, then at that point a build-up in oil inventories would be a blessing.

So I was very surprised when the initial tests weren't showing any tell-tale signs of a speculative bubble. If you want to talk about ideological bias, you could say that it was apparent since I was prepared to argue "trust the market" whether or not speculators were pushing up the price of oil. But my views on whether the speculators were responsible weren't driven by a preordained conclusion.

But back to the question at hand: Reader Joe Potts emailed me and asked if the apparent bursting of the oil bubble has made me revisit my arguments about speculators. I would definitely need to study the matter more carefully before giving a definitive answer, but here are my quick reactions:

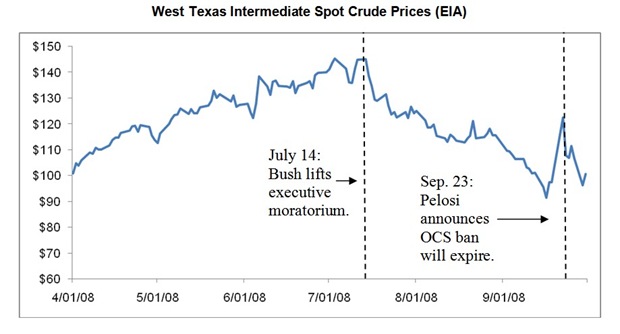

(1) The big swing in prices certainly looks like it has nothing to do with fundamentals, but keep in mind (a) the dollar fell sharply and then rebounded very sharply from September 07 - October 08; the graph of oil prices measured in euros or pounds wouldn't look nearly as bubblicious, (b) the prospects for future economic growth have completely collapsed during the period in question, and (c) the US removed the moratoria on billions of barrels of domestic reserves (see the surprising graph below). So when smart alecks say, "Oh, you told us it was supply and demand. Did those curves for oil really shift that much in 4 months?!" the answer is, "Maybe." When you throw in the fact that oil is famously price inelastic, then it is just possible that much of the apparent bubble is really due to changes in the fundamentals.

(2) Even if it were true that hedge funds and other institutional investors were pushing up oil prices during 2007 and the first half of 2008, nonetheless 95% of the people who "called" it were still spouting nonsense. In particular, they were acting as if the hedge funds could push the price up automatically and make guaranteed money--that's why the CFTC needed to step in and lay down the law to protect hapless motorists. The sudden collapse in oil prices shows that their worldview was rather flimsy.

(3) I would need to first run some back-of-the-envelope calculations to see how much wiggle room the factors I discussed in point (1) give me. If it still looks like I need to do some serious 'splainin, it occurs to me that there is a theoretical possibility that the typical "It's those greedy speculators!!" people would have missed, but also that I would have missed with my (somewhat) methodical process of elimination. What if the demand by end users (such as refiners) is fairly malleable, based on expectations of future prices? Something like, the refiners will buy 5 million bbl/day when the price is $90 per barrel, and they expect prices to remain at $90+ for at least the next 12 months. But if they consider $90 to be a ridiculously unsustainable price, then they only buy 4.5 mbd at that price.

I haven't worked this through yet, but it's something that neither side really considered. The people blaming "speculators" had in mind hedge funds or, for the more sophisticated analysts, they blamed the oil producers who cut production and "stockpiled" oil underground. But as I explained in the articles linked in the beginning of this post, the data just don't support either of those claims.

However, what if the "speculation" was being done by the actual end users? That would be indistinguishable (with the approach I was using) from saying, "Nah, physical oil demand is way up. There are no inventories accumulating." And yet, this case was clearly not what I had in mind when talking about the "fundamentals." (We are already getting into this gray area if we say that the lifting of the executive and then congressional bans on offshore drilling moved prices. Because obviously, if those policy changes have an immediate impact, it must be working through expectations. All along--even before it happened, mind you!--I expected the effect would come from producers increasing output, since they expected more competition from the US in ten years or whatever. But maybe that same mechanism was at play on the "fundamental" demand side too.)

In conclusion, I am not yet throwing in the towel and saying, "Yep, it was a speculative bubble." But if I do end up deciding that, I think it would be along the lines of point (3), since the logic in the earlier articles still seems solid to me.

Well, here's a chart of oil prices:

I think we can all agree, that looks pretty bubblicious.

So what gives? Well, the thing is, I still don't see any obvious mistakes in the chain of reasoning I used in the two articles linked above. And for the record, I didn't come to the analysis thinking, "OK, for political reasons it can't be the fault of hedge funds, so I have to work some Murphy Magic here and spin a story."

On the contrary, I initially thought it was speculators in the futures market driving up oil prices, especially since the take-off in commodities really kicked in when the Fed started cutting rates in September 07. (For example, the yr/yr change in monthly oil prices was actually negative until then, but afterward of course oil prices started exploding.) So I was coming to the analysis thinking speculators were holding prices up above the equilibrium price as determined by the "short-run fundamentals" (if you will), and I was prepared to explain why that was a good thing. E.g. if the US started bombing Iran, then at that point a build-up in oil inventories would be a blessing.

So I was very surprised when the initial tests weren't showing any tell-tale signs of a speculative bubble. If you want to talk about ideological bias, you could say that it was apparent since I was prepared to argue "trust the market" whether or not speculators were pushing up the price of oil. But my views on whether the speculators were responsible weren't driven by a preordained conclusion.

But back to the question at hand: Reader Joe Potts emailed me and asked if the apparent bursting of the oil bubble has made me revisit my arguments about speculators. I would definitely need to study the matter more carefully before giving a definitive answer, but here are my quick reactions:

(1) The big swing in prices certainly looks like it has nothing to do with fundamentals, but keep in mind (a) the dollar fell sharply and then rebounded very sharply from September 07 - October 08; the graph of oil prices measured in euros or pounds wouldn't look nearly as bubblicious, (b) the prospects for future economic growth have completely collapsed during the period in question, and (c) the US removed the moratoria on billions of barrels of domestic reserves (see the surprising graph below). So when smart alecks say, "Oh, you told us it was supply and demand. Did those curves for oil really shift that much in 4 months?!" the answer is, "Maybe." When you throw in the fact that oil is famously price inelastic, then it is just possible that much of the apparent bubble is really due to changes in the fundamentals.

(2) Even if it were true that hedge funds and other institutional investors were pushing up oil prices during 2007 and the first half of 2008, nonetheless 95% of the people who "called" it were still spouting nonsense. In particular, they were acting as if the hedge funds could push the price up automatically and make guaranteed money--that's why the CFTC needed to step in and lay down the law to protect hapless motorists. The sudden collapse in oil prices shows that their worldview was rather flimsy.

(3) I would need to first run some back-of-the-envelope calculations to see how much wiggle room the factors I discussed in point (1) give me. If it still looks like I need to do some serious 'splainin, it occurs to me that there is a theoretical possibility that the typical "It's those greedy speculators!!" people would have missed, but also that I would have missed with my (somewhat) methodical process of elimination. What if the demand by end users (such as refiners) is fairly malleable, based on expectations of future prices? Something like, the refiners will buy 5 million bbl/day when the price is $90 per barrel, and they expect prices to remain at $90+ for at least the next 12 months. But if they consider $90 to be a ridiculously unsustainable price, then they only buy 4.5 mbd at that price.

I haven't worked this through yet, but it's something that neither side really considered. The people blaming "speculators" had in mind hedge funds or, for the more sophisticated analysts, they blamed the oil producers who cut production and "stockpiled" oil underground. But as I explained in the articles linked in the beginning of this post, the data just don't support either of those claims.

However, what if the "speculation" was being done by the actual end users? That would be indistinguishable (with the approach I was using) from saying, "Nah, physical oil demand is way up. There are no inventories accumulating." And yet, this case was clearly not what I had in mind when talking about the "fundamentals." (We are already getting into this gray area if we say that the lifting of the executive and then congressional bans on offshore drilling moved prices. Because obviously, if those policy changes have an immediate impact, it must be working through expectations. All along--even before it happened, mind you!--I expected the effect would come from producers increasing output, since they expected more competition from the US in ten years or whatever. But maybe that same mechanism was at play on the "fundamental" demand side too.)

In conclusion, I am not yet throwing in the towel and saying, "Yep, it was a speculative bubble." But if I do end up deciding that, I think it would be along the lines of point (3), since the logic in the earlier articles still seems solid to me.

Comments:

Bob,

How about the fact that it was just plain old price inflation from years of Fed money printing, that was driving up all commodities?

When Bernanke stopped printing money this summer he killed what was close to becoming runaway inflation and killed (short term) inflationary expectations. And, indeed the accompanying financial crisis has resulted in deflationary pressure (short term) as the demand to hold cash balances climbs.

In my book, it wasn't a bubble as much as further evidence of the collapse of the dollar, given a short reprieve by Bernanke's halt to money printing activities this summer.

How about the fact that it was just plain old price inflation from years of Fed money printing, that was driving up all commodities?

When Bernanke stopped printing money this summer he killed what was close to becoming runaway inflation and killed (short term) inflationary expectations. And, indeed the accompanying financial crisis has resulted in deflationary pressure (short term) as the demand to hold cash balances climbs.

In my book, it wasn't a bubble as much as further evidence of the collapse of the dollar, given a short reprieve by Bernanke's halt to money printing activities this summer.

RW,

That's a good possibility, but again, how does that fit into the framework in which the "speculators vs. fundamentals" people were arguing? I think actually your point fits into my (3), because the pro-speculator crowd could say, "Yep, it was everyone speculating that prices would keep going up; the oil price got a little ahead of itself, so to speak." Whereas the "fundamental" crowd could say, "It wasn't a self-fulfilling prophecy; the investors had good reasons to think supply and demand--as measured in nominal dollars--were permanently shifted."

Do you see what I'm saying, RW? You're giving me a specific story to fill in my category (3), I think. And if you're right, that just shows the weakness in the dichotomy setup by the two camps (including me) during the run-up.

That's a good possibility, but again, how does that fit into the framework in which the "speculators vs. fundamentals" people were arguing? I think actually your point fits into my (3), because the pro-speculator crowd could say, "Yep, it was everyone speculating that prices would keep going up; the oil price got a little ahead of itself, so to speak." Whereas the "fundamental" crowd could say, "It wasn't a self-fulfilling prophecy; the investors had good reasons to think supply and demand--as measured in nominal dollars--were permanently shifted."

Do you see what I'm saying, RW? You're giving me a specific story to fill in my category (3), I think. And if you're right, that just shows the weakness in the dichotomy setup by the two camps (including me) during the run-up.

Don't forget about China stockpiling oil, especially diesel, in the run up to the Olympics. Combine that with the diesel supplies for repairing damage from the earthquake, and you have a lot of additional marginal demand, which drove up short term fundamentals.

On the flip side, oil was a bubble in the sense that it was riding on the back of the credit bubble and it's final implosion. As credit was sloshing around from place to place before it's final destruction, it ran to the last fundamentally strong story, that is, oil. So, was it a bubble? Yes and no. I would argue that it is a sign of things to come, that is, the fundamentals for expensive oil are still compelling, and this crisis even makes those fundamentals even better (or worse, in the sense that oil will become more expensive) as exploration is literally impossible to fund, and with oil prices this low, not economic.

On the flip side, oil was a bubble in the sense that it was riding on the back of the credit bubble and it's final implosion. As credit was sloshing around from place to place before it's final destruction, it ran to the last fundamentally strong story, that is, oil. So, was it a bubble? Yes and no. I would argue that it is a sign of things to come, that is, the fundamentals for expensive oil are still compelling, and this crisis even makes those fundamentals even better (or worse, in the sense that oil will become more expensive) as exploration is literally impossible to fund, and with oil prices this low, not economic.

Identification and measurement of STORAGE CAPACITY at every point between the wellhead and the consumer's fuel tank is essential is gauging the market's elasticity and the headroom that speculators (both pure and functional) actually have in timing their purchases and sales. Much effort goes into the estimation of reserves (in the ground). OTHER reserves, starting with things like the Strategic Petroleum Reserve, are vital in their effects on the volatility of prices.

Post a Comment

Subscribe to Post Comments [Atom]

<< Home

![]()

Subscribe to Posts [Atom]