Monday, April 12, 2010

Calling All Stragglers

I'm not sure if this will even work, but several weeks ago I made a dumb mistake and switched the RSS feed for my blog. We couldn't undo the mistake, but it occurred that maybe if I try making a post through Blogger (instead of the new Wordpress platform) people who are still using the old RSS feed can see this message.

Soooo, if you haven't seen the new blog posts, please manually go to the same URL and update your RSS feed. Send me an email if you have trouble.

Soooo, if you haven't seen the new blog posts, please manually go to the same URL and update your RSS feed. Send me an email if you have trouble.

Monday, March 15, 2010

Murphy Double Play

* At MasterResource I tut-tut Robert Frank's NYT column on climate change that scared the children. I use the latest Economic Report from the President (as in Obama), as well as a chart from the latest IPCC report (aka "the scientific consensus"), to show that the world is not ending, at least according to our trusted government and association-of-governments documents.

* At Mises I show the hidden paradox in standard free market arguments for drug legalization and against union thuggery. Specifically, a typical economic case for drug legalization will blame gang violence on the lack of contract enforcement (e.g. a drug dealer can't call the cops if he gets robbed), and free market economists will also usually say that unions can achieve above-market wage rates because the government doesn't intervene to protect "scabs" from picketers.

On the face of it, aren't these odd positions for a rabid free marketeer to take? In other words, s/he is arguing that there would be less gang violence, and a more coordinated labor market, if only the government would use its monopoly of courts and police more.

I resolve the paradox in my article.

* At Mises I show the hidden paradox in standard free market arguments for drug legalization and against union thuggery. Specifically, a typical economic case for drug legalization will blame gang violence on the lack of contract enforcement (e.g. a drug dealer can't call the cops if he gets robbed), and free market economists will also usually say that unions can achieve above-market wage rates because the government doesn't intervene to protect "scabs" from picketers.

On the face of it, aren't these odd positions for a rabid free marketeer to take? In other words, s/he is arguing that there would be less gang violence, and a more coordinated labor market, if only the government would use its monopoly of courts and police more.

I resolve the paradox in my article.

Knappenberger Catches the IPCC With Its Pants Down

Over at MasterResource, Chip Knappenberger (who is a published climate scientist, though he is ABD I believe) has a great post documenting the IPCC Fourth Assessment Report's treatment of Antarctic sea ice. Here is the intro:

Let me give one more hint: The post keeps getting better, the deeper you get into it, but you can't just skip to the punchline. You need to read the whole thing as it builds to the climax, and the noose tightens around the IPCC authors who were in charge of this particular section.

Some climate scientists have distanced themselves from the IPCC Working Group II’s (WGII’s) Fourth Assessment Report (AR4), Impacts, Adaptation, and Vulnerability, prefering instead the stronger hard science in the Working Group I (WGI) Report—The Physical Science Basis. Some folks have even gone as far as saying that no errors have been found in the WGI Report and the process in creating it was exemplary.I warn you that Chip's post is a bit long, and for full effect you need to read it carefully. But if you are at all interested in this issue--and you don't want to reflexively say "hoax! hoax!" just because you are a libertarian--I think Chip's post is well worth the effort.

Such folks are in denial.

As I document below, WGI did a poor job in regard to Antarctic sea ice trends. Somehow, the IPCC specialists assessed away a plethora of evidence showing that the sea ice around Antarctica has been significantly increasing—a behavior that runs counter to climate model projections of sea ice declines—and instead documented only a slight, statistically insignificant rise.

How did this happen? The evidence suggests that IPCC authors were either being territorial in defending and promoting their own work in lieu of other equally legitimate (and ultimately more correct) findings, were being guided by IPCC brass to produce a specific IPCC point-of-view, or both.

Let me give one more hint: The post keeps getting better, the deeper you get into it, but you can't just skip to the punchline. You need to read the whole thing as it builds to the climax, and the noose tightens around the IPCC authors who were in charge of this particular section.

Paul "W." Krugman

Krugman continues to outdo himself. In this article he somehow ends up saying: "In short, right now America has China over a barrel, not the other way around." Right, just like I have my credit card companies right where I want them.

Here's a fun experiment: Go through this Krugman column and replace "China" with "Iraqn," and "import surcharge" with "bomb the crud out of them." The Krugman op ed suddenly turns into a Max Boot piece.

Here's a fun experiment: Go through this Krugman column and replace "China" with "Ira

Sunday, March 14, 2010

Should Christians Support a Necessary Evil?

[CORRECTION within post, below.]

Kevin Clauson gave an interesting talk at the Austrian Scholars Conference concerning the apparent (but spurious in his mind) tension between evangelical political views and Austro-libertarianism. During the talk he described government as a "necessary evil" and cited Romans 13 to show that God had instituted civil authority, but that the sinful nature of men meant that government needed to be very limited.

Norman Horn in the Q&A raised a question along the lines of, "I happen to disagree with you that government is necessary, but let's put that aside. I'm interested in your acceptance of the very concept of a necessary evil."

Clauson reiterated his points about the sinful nature of man (making government necessary but at the same time very dangerous) and once again cited Romans 13. But then Norman explained that he wasn't challenging the existence of government, but rather the concept of a necessary evil. Then he said something like, "But earlier in the book of Romans he says, 'What shall we say then? Shall we do evil that God may work good from it? By no means!'"

[UPDATE: The following is wrong, I picked up the wrong passage when I tried to find what Norman was alluding to. Please read the comments to see a much better debate.] I think he was referring to Romans 6, and the translation here is not exactly how I remembered Norman making his point. In other words, the translation here (and the ones I'm used to) are not as clearly in conflict with someone who thinks there is such a thing as a necessary evil, i.e. that Christians could use an admittedly evil thing (the State) to effect a good outcome.

Anyway I am not sure myself how I feel about all this. According to my own arguments on this very blog, I think I would have to agree that the world itself is a necessary evil in God's plan.

Note that Norman could still argue that humans shouldn't use evil things as a way to effect good outcomes, even though God does that (e.g. Joseph's betrayal at the hands of his brothers). But I think Norman was trying to argue that the very notion of a necessary evil is nonsense.

Kevin Clauson gave an interesting talk at the Austrian Scholars Conference concerning the apparent (but spurious in his mind) tension between evangelical political views and Austro-libertarianism. During the talk he described government as a "necessary evil" and cited Romans 13 to show that God had instituted civil authority, but that the sinful nature of men meant that government needed to be very limited.

Norman Horn in the Q&A raised a question along the lines of, "I happen to disagree with you that government is necessary, but let's put that aside. I'm interested in your acceptance of the very concept of a necessary evil."

Clauson reiterated his points about the sinful nature of man (making government necessary but at the same time very dangerous) and once again cited Romans 13. But then Norman explained that he wasn't challenging the existence of government, but rather the concept of a necessary evil. Then he said something like, "But earlier in the book of Romans he says, 'What shall we say then? Shall we do evil that God may work good from it? By no means!'"

[UPDATE: The following is wrong, I picked up the wrong passage when I tried to find what Norman was alluding to. Please read the comments to see a much better debate.] I think he was referring to Romans 6, and the translation here is not exactly how I remembered Norman making his point. In other words, the translation here (and the ones I'm used to) are not as clearly in conflict with someone who thinks there is such a thing as a necessary evil, i.e. that Christians could use an admittedly evil thing (the State) to effect a good outcome.

Anyway I am not sure myself how I feel about all this. According to my own arguments on this very blog, I think I would have to agree that the world itself is a necessary evil in God's plan.

Note that Norman could still argue that humans shouldn't use evil things as a way to effect good outcomes, even though God does that (e.g. Joseph's betrayal at the hands of his brothers). But I think Norman was trying to argue that the very notion of a necessary evil is nonsense.

Friday, March 12, 2010

Why Supply-Siders Needs to Learn Austrian Business Cycle Theory

Murphy Demolished?

I actually don't have a problem with this lengthy review of New Deal revisionism (thanks to reader teqzilla for the tip), because the writer quotes me more than I think any other reviewer has done. I'm reading his stuff thinking, "Yep, yep, this guy Murphy makes a lot of sense." I don't recall "sniff"ing and being disgusted with things, the way the reviewer describes my book, but perhaps I need outside eyes to be objective.

I will probably write a response to this at some point, but it will have to wait for now...In the meantime, here's a good excerpt:

I will probably write a response to this at some point, but it will have to wait for now...In the meantime, here's a good excerpt:

But since the mobilization effort mandated such measures as price controls, the draft, and rationing of scarce materials such as rubber and steel for war production purposes, the whole thing was the foulest of economic abominations. “So the carefully constructed measures of ‘inflation-adjusted gross domestic output’ during the 1940s are about as meaningful as the economic statistics reported by the Soviet Union,” Murphy notes in disgust. “The government effectively made it illegal for market prices to signal how much inflation the Fed was pumping into the system.”

And so it is with all the economic measures of the grotesquely defiled Forties. Sure, the poor saps drafted into the Army or the female workers who thronged into war production factories might have thought things were turning around. But they were blind to how the pure model of laissez-faire was being molested! After all, Murphy explains, “there are other goods and services that those scarce resources could have produced, but which humans will now never enjoy because they were devoted to government projects.” Think of all the miniature golf facilities, nylon stockings and radios senselessly sacrificed just for the liberal vanity project of defeating fascism!

Likewise with the erstwhile layabouts now caught up by the draft—how could anyone count this as a legitimate form of employment? Suppose, for example, “that FDR announced in 1940 that in an effort to fight the Depression, all able-bodied unemployed men would be shipped to African jungles (where they faced lions and disease). That policy would have brought down the official unemployment rate,” Murphy sniffs, “yet it obviously would not have promoted actual economic recovery. Had FDR suggested something this monstrous as a ‘cure’ for mass unemployment, citizens would have rightfully recoiled in horror.”

Indeed, one can almost picture Murphy himself, after typing up such infamies, smiting his breast, slumping alongside his laptop, lifting his head heavenward only to convulsively shout, “Unclean! Unclean!” After all, had the market approved of the war, it could by itself have instructed wartime production facilities where to allocate resources, by the magic of the price mechanism. “Precisely because World War II was an unprecedented event, there were no ‘experts’ on transforming civilian production to military production on this scale. When it comes to motivating millions of people to brainstorm and quickly come up with better ways to make a mousetrap (or tank), nothing beats the profit-driven market economy.”

Back in consensual reality, however, the Second World War doesn’t actually reduce to a perverse safari outing. There was a Japanese attack on a U.S. naval base, and a massive German effort to conquer the West and spread racial genocide. Oh, and the “pecuniary” stakes were far from negligible, as well, with a war-driven Nazi command economy curiously indifferent to the domestic production needs of Poland, France, Belgium, the Balkan states, and so on. A laissez-faire outlook among the Allied powers, in other words, would almost certainly have resulted in a fascist triumph. (Even more inconveniently, the killing blow to Nazi imperialism was delivered by the most hatefully statist command economy of them all, Stalinist Russia.)

Thursday, March 11, 2010

Trade Deficits and Fiat Currencies

Wow, you know I must be super busy if I forgot to blog my Mises Daily on Monday. It was "Trade Deficits and Fiat Currencies," showing the connection between the two. I both praise and critique the author of The Creature From Jekyll Island.

This morning I gave my talk at the Denver Petroleum Club. One of my opening slides talked about the IER D.C. office and how I didn't have a picture of it because we had recently moved, so instead I said this shot represented our efforts. I didn't get as big a laugh as I was hoping--perhaps because it was an older crowd--but other than that things went well.

Then I hopped on a plane to Atlanta, retrieved my car from the Economy lot, and drove down to Auburn. I'm about to crash and then tomorrow morning I give the Hayek lecture at the Austrian Scholar's Conference.

I think I actually get to sleep Friday night. I can't wait.

This morning I gave my talk at the Denver Petroleum Club. One of my opening slides talked about the IER D.C. office and how I didn't have a picture of it because we had recently moved, so instead I said this shot represented our efforts. I didn't get as big a laugh as I was hoping--perhaps because it was an older crowd--but other than that things went well.

Then I hopped on a plane to Atlanta, retrieved my car from the Economy lot, and drove down to Auburn. I'm about to crash and then tomorrow morning I give the Hayek lecture at the Austrian Scholar's Conference.

I think I actually get to sleep Friday night. I can't wait.

Sunday, March 7, 2010

I Write Six Days a Week, and Rest on the Sabbath

Lately I have tried to do a better job of "observing the Sabbath," meaning that I try not to work on Sundays. As a consultant, I never have a vacation. At any given time, there is always something I could be doing (or at least get the wheels moving) to bring in more revenue.

Currently my compromise is that I allow myself to read "worky" things, and I allow myself to work on the household budget, but I don't produce anything that someone else is paying me for. Eventually I will get to the point where I truly "don't work on Sundays."

Similar to the rule about tithing, the same holds for observing the Sabbath. Paradoxically, I have found that I get more done in a seven-day period, when I know during the week that I am not going to allow myself to do "real work" on Sunday. Presumably this has to do with the fact that you really can't go nonstop for a week without taking mini-breaks, and you use your time more effectively from Monday through Saturday if you know you are going to really take Sunday off.

Currently my compromise is that I allow myself to read "worky" things, and I allow myself to work on the household budget, but I don't produce anything that someone else is paying me for. Eventually I will get to the point where I truly "don't work on Sundays."

Similar to the rule about tithing, the same holds for observing the Sabbath. Paradoxically, I have found that I get more done in a seven-day period, when I know during the week that I am not going to allow myself to do "real work" on Sunday. Presumably this has to do with the fact that you really can't go nonstop for a week without taking mini-breaks, and you use your time more effectively from Monday through Saturday if you know you are going to really take Sunday off.

Friday, March 5, 2010

Update

Hey kids, just to let you know, I am swamped with "real work" for the foreseeable future. (I'm even busier than this guy.) Also, if it works out, I will be migrating the blog to Wordpress during my hiatus.

For anyone in the area, I am giving a talk at the Denver Petroleum Club on Thursday morning (will they be expecting a troll?), and then it's off to Auburn for the Austrian Scholars Conference [.pdf]. My intelligence sources indicate that there is a new karaoke bar in Auburn, which features karaoke every night of the week.

For anyone in the area, I am giving a talk at the Denver Petroleum Club on Thursday morning (will they be expecting a troll?), and then it's off to Auburn for the Austrian Scholars Conference [.pdf]. My intelligence sources indicate that there is a new karaoke bar in Auburn, which features karaoke every night of the week.

Wednesday, March 3, 2010

Boosting Productivity By Ditching the Boob Tube

Lately people have been asking me how I get "so much" done. This always strikes me as funny since, at any given time, I'm usually behind on several projects.

One obvious thing is that we have not had a TV in our house since we left Hillsdale. (And even then, we didn't have cable and were on a lake so we had bad reception.) That literally gives you an extra two hours a day at least to get work done. Even if you're not watching it, someone else probably is. Imagine if one class of comparable students taking a test had a TV on in the background, while another had peace and quiet. Which group would score better?

When I had a TV in grad school, I used to wind down by watching Seinfeld and other reruns late at night after the long train ride from NYU to my apartment in New Jersey. Asking me at the time to give that up would have been like making me become a vegetarian.

But once you go through withdrawal, you will be amazed at how ridiculous TV is. If you have had one all along, you probably haven't noticed just how ludicrous it has become. I only see it now when I visit someone's house or stay in a hotel, so I see it in short samples spread out over weeks.

I'm not saying this as a prude, just making an observation: Modern American cable television is literally pornographic. If you flip through the channels, you will see cleavage or a sexually suggestive scenario (like a crime show where the victim is a stripper or a prostitute or something) on about every 5th channel, depending on the time of day. Fueled by FOX, every news show has to have a really attractive person on the camera at all times if possible.

And don't get me started on what's happened to wrestling since my younger brother used to watch Macho Man Savage and the Undertaker.

One obvious thing is that we have not had a TV in our house since we left Hillsdale. (And even then, we didn't have cable and were on a lake so we had bad reception.) That literally gives you an extra two hours a day at least to get work done. Even if you're not watching it, someone else probably is. Imagine if one class of comparable students taking a test had a TV on in the background, while another had peace and quiet. Which group would score better?

When I had a TV in grad school, I used to wind down by watching Seinfeld and other reruns late at night after the long train ride from NYU to my apartment in New Jersey. Asking me at the time to give that up would have been like making me become a vegetarian.

But once you go through withdrawal, you will be amazed at how ridiculous TV is. If you have had one all along, you probably haven't noticed just how ludicrous it has become. I only see it now when I visit someone's house or stay in a hotel, so I see it in short samples spread out over weeks.

I'm not saying this as a prude, just making an observation: Modern American cable television is literally pornographic. If you flip through the channels, you will see cleavage or a sexually suggestive scenario (like a crime show where the victim is a stripper or a prostitute or something) on about every 5th channel, depending on the time of day. Fueled by FOX, every news show has to have a really attractive person on the camera at all times if possible.

And don't get me started on what's happened to wrestling since my younger brother used to watch Macho Man Savage and the Undertaker.

Potpourri

* This blew me away: Joe Salerno discusses Murray Rothbard's call for anti-statists to pull their money out of the commercial banking system. OK, so let's suppose Austro-libertarians agree that they should stop the inflating Fed in its tracks by boycotting the commercial banks. But what is the free market alternative? (Don't think tax-qualified retirement plans.) It would be nice if it already existed, in a time-tested financial product that Austro-libertarians already have an affinity for. Well we can dream.

* Sometimes even Joe Romm has to backpedal. Debate! Debate!

* Why I read EPJ: The real explanation for the fate of Charlie Rangel.

* Here's the audio of my talk at Jekyll Island, titled, "Only the Austrians Can Explain Depressions." Some jokes in the beginning, and then Scott Sumner bashing in the middle.

* I don't believe in Profile updates and all that jazz, but Vijay Boyapati had a cool Gandhi quote the other day: "The ideally non-violent state will be an ordered anarchy. That State is the best governed which is governed the least."

* Sometimes even Joe Romm has to backpedal. Debate! Debate!

* Why I read EPJ: The real explanation for the fate of Charlie Rangel.

* Here's the audio of my talk at Jekyll Island, titled, "Only the Austrians Can Explain Depressions." Some jokes in the beginning, and then Scott Sumner bashing in the middle.

* I don't believe in Profile updates and all that jazz, but Vijay Boyapati had a cool Gandhi quote the other day: "The ideally non-violent state will be an ordered anarchy. That State is the best governed which is governed the least."

Onion Reports: Obama Caught Lip-Synching Speech

This made me chuckle three separate times, and that's good enough for government-bashing work. (HT2 Viresh Amin)

A Picture Is Worth a Thousand Lies

This is hilarious. Lew Rockwell sends along the Cleveland Fed's latest video in its, "Really bad drawings, real simple explanation" series (check the link if you think I'm making up the title). It's 9 minutes long so maybe that's too much for you, but at least watch it through 3:55 to see the graph of how the Fed maintains a stable purchasing power of the dollar from 1 - 10 years out.

If someone has a lot of free time on his or her hands, it would be hilarious to do a parody of this, explaining how the CIA works.

In closing, I must say that the tone of this video intrigues me. You get the sense that the actual Fed staffers know full well they're participating in something shady. For example listen in the beginning when they introduce Ben Bernanke, or at the very end when they say, "However you feel about the Fed..."

If someone has a lot of free time on his or her hands, it would be hilarious to do a parody of this, explaining how the CIA works.

In closing, I must say that the tone of this video intrigues me. You get the sense that the actual Fed staffers know full well they're participating in something shady. For example listen in the beginning when they introduce Ben Bernanke, or at the very end when they say, "However you feel about the Fed..."

Tuesday, March 2, 2010

Bernanke Still Breaking Records

Reports of the imminent collapse of the monetary base have thus far been greatly exaggerated... I'm not saying that Bernanke was lying when he claimed the base would start shrinking real soon, I just want to point out that it wouldn't be the first time.

This Is Potentially the Screwiest GDP Chart I've Ever Seen

Paul Krugman links to Mark Thoma who in turn cribs from the Federal Reserve Bank of San Fran to give us...

The definition of "potential GDP" comes from the San Fran bank:

Then, at no time whatsoever during the housing and stock market boom (except maybe a little blip in 2006) was actual GDP higher than potential. According to the CBO's calculation (which is where SF got the potential GDP number), the US economy in the year, say, 2005 was in a perfectly sustainable configuration. We could have repeated the experience of 2005 indefinitely, if only we had implemented the proper policies.

And now, of course, there is no reason for output to have fallen in the current recession. It's just that aww shucks aggregate demand collapsed for some nonsensical reason, and now we're stuck with a trillion dollars less in output per year than we ought to be enjoying.

There are two lessons from all this:

(1) Mainstream macroeconomists have a very very crude notion of the structure of production. Their models literally cannot handle the possibility that an unsustainable boom from 2002-2006 could have physically necessitated a drop in measured output from 2007-2008.

(2) As the persistent von Pepe keeps reminding me, the mainstream focus on CPI as the measure of "inflation" is wrong. As the chart above shows, people who think the economy is in great shape so long as CPI grows at a moderate pace can often fall flat on their faces.

The definition of "potential GDP" comes from the San Fran bank:

Potential output is not a measure of maximum output that can be achieved, but instead maximum sustainable output. As such, it is the level of real GDP that is consistent with stable inflation. When actual real GDP is running higher than potential GDP, the economy is said to be producing above full capacity.Now look back at that chart, to see if we like the implications of this typical macro way of looking at things. Actual GDP was higher than potential GDP during the recession of 2000-2001; isn't that a bit weird?

Then, at no time whatsoever during the housing and stock market boom (except maybe a little blip in 2006) was actual GDP higher than potential. According to the CBO's calculation (which is where SF got the potential GDP number), the US economy in the year, say, 2005 was in a perfectly sustainable configuration. We could have repeated the experience of 2005 indefinitely, if only we had implemented the proper policies.

And now, of course, there is no reason for output to have fallen in the current recession. It's just that aww shucks aggregate demand collapsed for some nonsensical reason, and now we're stuck with a trillion dollars less in output per year than we ought to be enjoying.

There are two lessons from all this:

(1) Mainstream macroeconomists have a very very crude notion of the structure of production. Their models literally cannot handle the possibility that an unsustainable boom from 2002-2006 could have physically necessitated a drop in measured output from 2007-2008.

(2) As the persistent von Pepe keeps reminding me, the mainstream focus on CPI as the measure of "inflation" is wrong. As the chart above shows, people who think the economy is in great shape so long as CPI grows at a moderate pace can often fall flat on their faces.

Monday, March 1, 2010

The Futility of a Violent Revolution

I want to give a quick summary of my views on violent resistance to a tyrannical government, in light of the Austin plane attack and the (possible) attack on a Utah IRS facility.

* There is a big difference between arming yourself and saying, "If they come onto my property, it's show time" versus, "I am going to fly my plane into a government office." If you're trying to win converts, the former is a lot more likely to garner sympathy than the latter.

* Proponents of violent resistance have in mind the idea that if we could just get x million fellow citizens to think like us and stand up to Big Brother, we'd eventually win after they killed y million of us. Well OK, but if we had x million fellow citizens who thought like us, then I submit it wouldn't take violence. They could just stop paying taxes and see what happened. The results would be the same--eventual crumbling of the empire--but with a lot less bloodshed.

* People (like the Austin pilot) who think it's smart strategy to provoke the government into doing something awful because then the people will rise up, are being awfully optimistic about the mass of Americans they otherwise refer to as "the sheeple." Remember Waco? How much more awful would the government have to be? But did the average American go buy a long gun and renew his membership in the John Birch society? Of course not. Most Americans just needed to hear a TV anchor give the official explanation. "Oh OK, yeah I guess that makes sense. If I were in charge of rescuing a bunch of children from abusive parents, I'd probably send in chemical weapons and tanks too. Too bad those kids had religious nutjob parents and got burned up."

Last point:

* People often invoke the Founding Fathers. Yes they were brave and they fought a war to free the country. And yet, many of the same people who love the Founding Fathers go on to chastise present-day Americans by saying, "Our nation of wimps now have a level of taxation far higher than the colonists endured under King George." Hmm there are two ways to interpret this. One is to say, "It's time for another bloodletting!" Another is to say, "Hmm maybe the violent American Revolution wasn't such a hot idea after all."

* There is a big difference between arming yourself and saying, "If they come onto my property, it's show time" versus, "I am going to fly my plane into a government office." If you're trying to win converts, the former is a lot more likely to garner sympathy than the latter.

* Proponents of violent resistance have in mind the idea that if we could just get x million fellow citizens to think like us and stand up to Big Brother, we'd eventually win after they killed y million of us. Well OK, but if we had x million fellow citizens who thought like us, then I submit it wouldn't take violence. They could just stop paying taxes and see what happened. The results would be the same--eventual crumbling of the empire--but with a lot less bloodshed.

* People (like the Austin pilot) who think it's smart strategy to provoke the government into doing something awful because then the people will rise up, are being awfully optimistic about the mass of Americans they otherwise refer to as "the sheeple." Remember Waco? How much more awful would the government have to be? But did the average American go buy a long gun and renew his membership in the John Birch society? Of course not. Most Americans just needed to hear a TV anchor give the official explanation. "Oh OK, yeah I guess that makes sense. If I were in charge of rescuing a bunch of children from abusive parents, I'd probably send in chemical weapons and tanks too. Too bad those kids had religious nutjob parents and got burned up."

Last point:

* People often invoke the Founding Fathers. Yes they were brave and they fought a war to free the country. And yet, many of the same people who love the Founding Fathers go on to chastise present-day Americans by saying, "Our nation of wimps now have a level of taxation far higher than the colonists endured under King George." Hmm there are two ways to interpret this. One is to say, "It's time for another bloodletting!" Another is to say, "Hmm maybe the violent American Revolution wasn't such a hot idea after all."

Bloomberg Writer Blasts British Keynesianism

This is a pretty uppity article by Matthew Lynn on Bloomberg (HT2 Jeff Tucker):

The U.K. has been in Keynes overdrive for the past 18 months. The budget deficit is already more than 12 percent of gross domestic product, on a par with Greece. And while the Greeks are cutting spending, the British deficit is widening. Figures for January showed another fiscal blowout. At the same time, interest rates have been slashed to 0.5 percent. And the pound has slumped in value, which is supposed to boost demand for British goods, and help close the trade gap.

Just about everything possible has been done to encourage consumption. The results have been miserable.

Retail sales excluding gasoline in January fell 1.2 percent from the previous month, twice as much as economists forecast. The number of people receiving unemployment benefits jumped to 1.64 million in January, the highest level since April 1997. The yield on U.K. government debt is now higher than on Spanish or Italian bonds, a sure sign that investors are losing faith in the country’s ability to pay its debts. The inflation rate has also accelerated to 3.5 percent.

Triple Whammy

In reality, Britain has the worst of all possible worlds: a stagnant economy, a crippling budget deficit and rising prices.

The Keynesian consensus is that things would have been far worse without the stimulus provided by government. And if the economy isn’t pumped up with inflated demand, it will collapse back into recession. If it’s not working, that just proves the stimulus should be even larger.

It is the argument quacks always push: If the medicine isn’t working, increase the dosage.

JFK, Blown Away, What Else Do I Have to Say?

Viresh Amin sends this very interesting snippet. Does anyone know what the official response to this is?

Incidentally, I did a decent amount of research over the summer and concluded that there was more than one shooter. I'm not saying I have a theory as to who shot JFK, just that I am confident the official story is bogus.

I will write up my case at some point, but it will take a lot of my time. I have to get someone to take a diagram from a book and translate it into a computer shot, etc.

Incidentally, I did a decent amount of research over the summer and concluded that there was more than one shooter. I'm not saying I have a theory as to who shot JFK, just that I am confident the official story is bogus.

I will write up my case at some point, but it will take a lot of my time. I have to get someone to take a diagram from a book and translate it into a computer shot, etc.

Hazmat Team Called to IRS Building in Utah

Details are still sketchy, but apparently two people were carried out on stretchers from an IRS facility and a Hazmat team was called in.

If this turns out to be another attack, let me reiterate my position: This is foolish. Ask yourself this: Why does it even make sense for the government to engage in "false flag" operations (whether or not you think it actually does this)? Because this allows the government to expand its power over a terrified citizenry.

I grant you, average people are less scared from attacks on the IRS as opposed to, say, the subway. But violence is the government's game. I strongly disagree with the strategy--let alone the morality--of those who think it's time to fight the US government.

If this turns out to be another attack, let me reiterate my position: This is foolish. Ask yourself this: Why does it even make sense for the government to engage in "false flag" operations (whether or not you think it actually does this)? Because this allows the government to expand its power over a terrified citizenry.

I grant you, average people are less scared from attacks on the IRS as opposed to, say, the subway. But violence is the government's game. I strongly disagree with the strategy--let alone the morality--of those who think it's time to fight the US government.

Inventories Don't Kill Growth--People Kill Growth

[UPDATE below.]

This is an esoteric piece, but is actually one of my personal favorites. I was struggling with this notion of an "inventory bump" in GDP growth for a while, and I resolved the issues (at least to my own satisfaction) in this article. So if you have always been vaguely uncomfortable with people attributing percentages of GDP growth to inventory adjustments, this one's for you. From the conclusion:

UPDATE: David R. Henderson has a good piece on "GDP fetishism" at EconLib today. Something isn't quite clicking for me in his example of the government paying $10 billion to workers who dig holes and then fill them up. David argues that if the workers get paid $10/hour for work that they would only have been willing to do for at least $6, then only $4 billion of "well-being" has been created on net, once we take into account the loss of leisure. But isn't this too an overstatement, since the workers only value the wages because of the actual goods and services they will be able to buy (and hence redistribute away from everyone else)? Maybe David is capturing that in his categories of price inflation or future tax hikes. Anyway, it's a good article.

This is an esoteric piece, but is actually one of my personal favorites. I was struggling with this notion of an "inventory bump" in GDP growth for a while, and I resolved the issues (at least to my own satisfaction) in this article. So if you have always been vaguely uncomfortable with people attributing percentages of GDP growth to inventory adjustments, this one's for you. From the conclusion:

The textbook GDP equation is not false; it is a tautology and so of course it is true. Nonetheless, it is a destructive framework for thinking about macroeconomic events. Abuse of the equation leads economists and pundits to blame savings and praise reckless consumption, to hate imports and love exports, and (in principle) to attribute a doubling in the flow of goods coming out of factories to a nonchange in the level of a nonexistent stock of inventory.The part I've just underlined is the contribution of the article; I came up with an easy numerical illustration showing that the standard GDP logic leads to that absurd possibility.

UPDATE: David R. Henderson has a good piece on "GDP fetishism" at EconLib today. Something isn't quite clicking for me in his example of the government paying $10 billion to workers who dig holes and then fill them up. David argues that if the workers get paid $10/hour for work that they would only have been willing to do for at least $6, then only $4 billion of "well-being" has been created on net, once we take into account the loss of leisure. But isn't this too an overstatement, since the workers only value the wages because of the actual goods and services they will be able to buy (and hence redistribute away from everyone else)? Maybe David is capturing that in his categories of price inflation or future tax hikes. Anyway, it's a good article.

Sunday, February 28, 2010

A Snapshot of My Conversion

I caught a really bad cold on Jekyll Island so I am going to make this a brief post. After the festivities last night, some of the young LvMI aficionados offered to buy me drinks if I didn't go back to my room. I considered the offer and texted my wife, "I believe the children are our future..."

Anyway, one of them was an atheist and asked me what made me convert. (I too had called myself a "devout atheist" in undergrad, and now I call myself a born-again Christian.) People ask me this a lot, so let me give the very quick summary of how my beliefs evolved.

(1) I can't go into the details here, but I went through a very powerful experience in which I experienced firsthand how much one's beliefs can influence perception. I had always known corny stuff like, "If you want to win the championship, you have to visualize success" or, "The guy who gets the girl is the guy who knows he's getting the girl." But I'm talking about much stronger stuff here, like having huge hives on your skin if you're worried about something.

(2) This newfound knowledge about how much you "create your own reality" made me really understand how it was possible that if a devout Jew truly believed the Messiah had just healed him, that he would actually be healed (of his lameness, leprosy, etc.). Note that at this point I was still an atheist. I just thought that I had figured out the trick. I no longer had to assume there was some guy Jesus who said some neat things, and then his followers invented a bunch of stories to make others pay attention. No, now things made a lot more sense: I thought there had been this guy Jesus who was earnest but had been raised in an unscientific culture, and he really believed he was God. Since he was so confident, he convinced a bunch of other people too. And you can't blame them; he was literally healing people on the spot. But it wasn't a miracle or magic; it was all due to the power of the human mind over the physical body, which I had only recently discovered.

(3) At some point (there's a lot more to the story) it occurred to me that if there were a God and He were to become incarnate as a man etc., that things would appear exactly as my atheistic investigations had revealed. In other words, what more do you want than a guy who goes around healing people, preaching the good news of the kingdom of God, etc.?

I don't expect the above to persuade anybody who thinks psychomatic medicine is some New Age touchy-feely thing, and that, "If you're sick you need some good drugs and maybe a CAT scan." But for whatever it's worth, it was the path that led from my atheism to theism.

Anyway, one of them was an atheist and asked me what made me convert. (I too had called myself a "devout atheist" in undergrad, and now I call myself a born-again Christian.) People ask me this a lot, so let me give the very quick summary of how my beliefs evolved.

(1) I can't go into the details here, but I went through a very powerful experience in which I experienced firsthand how much one's beliefs can influence perception. I had always known corny stuff like, "If you want to win the championship, you have to visualize success" or, "The guy who gets the girl is the guy who knows he's getting the girl." But I'm talking about much stronger stuff here, like having huge hives on your skin if you're worried about something.

(2) This newfound knowledge about how much you "create your own reality" made me really understand how it was possible that if a devout Jew truly believed the Messiah had just healed him, that he would actually be healed (of his lameness, leprosy, etc.). Note that at this point I was still an atheist. I just thought that I had figured out the trick. I no longer had to assume there was some guy Jesus who said some neat things, and then his followers invented a bunch of stories to make others pay attention. No, now things made a lot more sense: I thought there had been this guy Jesus who was earnest but had been raised in an unscientific culture, and he really believed he was God. Since he was so confident, he convinced a bunch of other people too. And you can't blame them; he was literally healing people on the spot. But it wasn't a miracle or magic; it was all due to the power of the human mind over the physical body, which I had only recently discovered.

(3) At some point (there's a lot more to the story) it occurred to me that if there were a God and He were to become incarnate as a man etc., that things would appear exactly as my atheistic investigations had revealed. In other words, what more do you want than a guy who goes around healing people, preaching the good news of the kingdom of God, etc.?

I don't expect the above to persuade anybody who thinks psychomatic medicine is some New Age touchy-feely thing, and that, "If you're sick you need some good drugs and maybe a CAT scan." But for whatever it's worth, it was the path that led from my atheism to theism.

Thursday, February 25, 2010

Scott Sumner's Money Illusions

I believe it was the acerbic von Pepe who said to me over email that Scott Sumner was right--the focus on money was an illusion. (This was a backhanded compliment, to say the least.) I tweaked it a bit for my title...

Lately Scott has been giving us sneak peeks at his book on the Great Depression (e.g. here). Scott's big thing is that the Fed needs to keep nominal GDP (NGDP) growing in order to stave off calamities. Scott admits there are other "real" shocks that can occur, such as a giant tax hike. But he's saying that in addition to all that, if the Fed doesn't print enough money to offset a huge increase in the demand to hold cash (for whatever reason it occurs), then that will be an additional kick to the economy. In particular, Scott thinks it was the Fed's timidity that caused the Great Depression, as well as the financial crisis of the fall of 2008.

So step 1, I went to the old Austrian workhorse, the depression of 1920-1921. Based on a site that a reader kindly dug up, we learn that the drop in nominal GDP from 1920-1921 was (almost) 17%. That was as big as any single-year drop during the Great Depression, except for the catastrophic year 1931-1932.

So the question is, would anybody say that the economy in 1931 was better than it was in 1921? According to Scott's theory, you might think that would be the case, since nominal GDP had fallen more sharply from 1920-1921 than from 1929-1930 (down 12%) or from 1930-1931 (down a little more than 16%). Unemployment was 8.7% in 1930, and had risen to 16.3% by 1931. In contrast, unemployment was 11.7% in 1921, but then it dropped down to 6.7% by 1922 and then 2.4% by 1923.

Now in fairness to Scott, he could say it is a cumulative matter, and in fact the figures above support his story. In other words (he could say) the reason unemployment in 1931 was higher than in 1921 (16.3% vs. 11.7%) was that nominal GDP had fallen a cumulative 26% from 1929-1931. So even though the one-year drop in NGDP from 1920-1921 was bigger than any single year drop up through 1931, it was the back to back drops of 1929 and 1930 that broke the back of the economy.

OK in and of itself, that's plausible enough. But how does Scott explain our current crisis? Assuming my late night calculations from the hotel room are correct, nominal GDP fell about 1.3% from 2008-2009. So how in the heck does that give us a ~10% unemployment rate? (You might ask, "What about the cumulative fall from 2007-2009?" But don't, because GDP in 2008 was higher than in 2007.)

Now maybe Scott would come back and refine the growth rates, and show that something happened in the 3rd quarter of 2008 that my annual figures above are smoothing out of existence. OK fine, but I don't think there's any way Scott is going to generate a recent fall in nominal GDP anywhere close the (almost) 17% one-year drop from 1920-1921. And yet, assuming the stats are measuring the same thing, the unemployment back then was just a point or two higher than it has been in our time.

Now let's move on to the decisive issue. Over email I asked Scott about these things, and he said (reproducing with permission), "Yes, there was a huge drop in NGDP in 1921, but I don't see where you are going with this. I agree with the Austrian view that a sharp fall in NGDP is a bad thing, and 1921 certainly supports that, as does 1929-33, when NGDP fell in half. I'm curious to hear your take on it."

So I said, "OK, I'm saying why did the economy escape a decade of depression in the 1920s--in fact had the Roaring 20s--when in the beginning, the 1920-1921 crash was worse (according to your theory) than the Great Depression crash? Did the Fed start targeting NGDP in 1921?"

Then Scott replied:

Scott explained: "The [monetary] Base fell sharply in 1921, and rose sharply in 1922."

OK for those who are still with me, let me show you how difficult it is to square the numbers on monetary base growth to fit Scott's narrative from above.

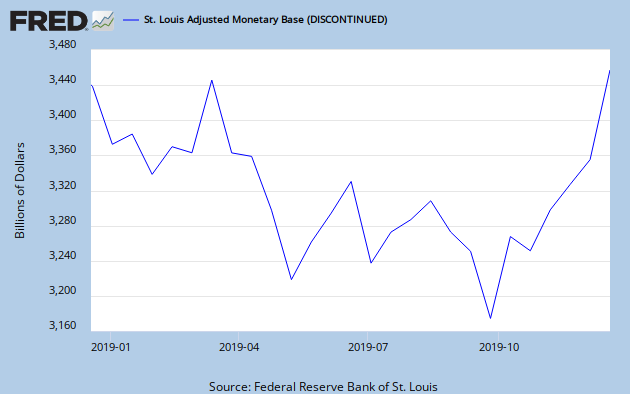

In the chart below, I have taken the St. Louis Fed's "Adjusted Monetary Base" series, the non-seasonally adjusted one. The data is monthly, which made it hard to see broad trends. So what I first did was construct quarterly averages out of the monthly data.

Then, I constructed 6-month growth rates for each quarter. So for example, the entry for 1920 1Q is 16.3%. What that means is that the average monetary base level in the 1st quarter of 1920 was 7.86% higher than the level in 3Q 1919. Since the base by 1st Q 1920 had grown 7.86% over the past 6 months, that works out to an annualized growth rate of monetary base of 16.3%. OK?

Now that you understand what the growth rates mean, check out this table:

I've put the significant money tightening periods in red, and the loosening periods in green. Now pretend for a minute that you knew nothing of the time periods, and you were applying Scott's theory. You want to predict which periods have the worst recessions.

OK the biggest reduction in monetary base occurs in 1921. It's true, the drop in 1937 is bad, but clearly the 1921 drop is worse. And the drop in 2008 is...oh wait, there was no drop in base. You just saw a slowdown in its growth.

Now at this point, we would expect the worst depression in US history to be in 1921, the second worst to be in 1937, and the third worst in 1930. We wouldn't even expect there to be a depression in 2008. (You can't see it in the excerpts I've given you, but there were other periods post-WW2 where monetary base actually fell or grew very anemically, and yet I don't think [off the top of my head] there were bad recessions in those periods. Clearly not "the worst Depression since WW2" which is what we are currently experiencing.)

OK let's be fair to Scott. He could argue that we need to look at the Fed's rescue of the economy in 1922, when (per Scott's email) monetary base grew rapidly. So we should expect to see the most phenomenal growth in monetary base in 1922, in order to counteract the huge restriction in the base in 1921. Otherwise, it would remain a mystery how the economy bounced back so quickly in 1922.

Uh oh. My measure of base growth was negative through the first half of 1922. And then even when it picked up, the highest it hit was 11.1% in the 4th quarter of 1922. Remember, unemployment had dropped about five percentage points--falling about in half--from 1921 to 1922.

So if the second-half spurt in 1922 explains the dramatic recovery--and indeed paved the way for the Roaring Twenties--then what was the problem in late 1931? The growth in monetary base then was much bigger than in late 1922. And yet we all know that unemployment continued to rise.

A similar puzzle occurs when we look at the huge, and consecutive, growth rates in 1938 and 1939. But unemployment was 19% in 1938, and was still 14.6% in 1940. Scott can give a story about "long and variable lags" to blame the spike in unemployment in 1938 on the monetary contraction in 1937, but how can he explain the post-1921 recovery by monetary base spurts that are pipsqueaks compared to the huge injections frmo 1938-1940?

Up till this point, Scott could maybe get by with a story that involved judicious use of cumulative effects etc. But look now to the green cells in late 2008 and early 2009. !!

I submit that Scott has fallen prey to a money illusion. Of course it can screw things up if our fractional reserve system allows a huge contraction in the money supply when other things are falling apart in the real economy. But just look at the 1920-1921 episode compared to 2008-2009. It is unreasonable to say the basic cause of our current malaise is that the Fed tightened up in 2008 and then didn't open the spigots enough after the crisis set in. The numbers aren't even in the right ZIP code for that explanation.

Back to you, Scott.

(NOTE: I am writing this from a hotel room. I reserve the right to change the numbers above in case I googled the wrong unemployment rate for a certain year, or screwed up the division for computing nominal GDP losses.)

Lately Scott has been giving us sneak peeks at his book on the Great Depression (e.g. here). Scott's big thing is that the Fed needs to keep nominal GDP (NGDP) growing in order to stave off calamities. Scott admits there are other "real" shocks that can occur, such as a giant tax hike. But he's saying that in addition to all that, if the Fed doesn't print enough money to offset a huge increase in the demand to hold cash (for whatever reason it occurs), then that will be an additional kick to the economy. In particular, Scott thinks it was the Fed's timidity that caused the Great Depression, as well as the financial crisis of the fall of 2008.

So step 1, I went to the old Austrian workhorse, the depression of 1920-1921. Based on a site that a reader kindly dug up, we learn that the drop in nominal GDP from 1920-1921 was (almost) 17%. That was as big as any single-year drop during the Great Depression, except for the catastrophic year 1931-1932.

So the question is, would anybody say that the economy in 1931 was better than it was in 1921? According to Scott's theory, you might think that would be the case, since nominal GDP had fallen more sharply from 1920-1921 than from 1929-1930 (down 12%) or from 1930-1931 (down a little more than 16%). Unemployment was 8.7% in 1930, and had risen to 16.3% by 1931. In contrast, unemployment was 11.7% in 1921, but then it dropped down to 6.7% by 1922 and then 2.4% by 1923.

Now in fairness to Scott, he could say it is a cumulative matter, and in fact the figures above support his story. In other words (he could say) the reason unemployment in 1931 was higher than in 1921 (16.3% vs. 11.7%) was that nominal GDP had fallen a cumulative 26% from 1929-1931. So even though the one-year drop in NGDP from 1920-1921 was bigger than any single year drop up through 1931, it was the back to back drops of 1929 and 1930 that broke the back of the economy.

OK in and of itself, that's plausible enough. But how does Scott explain our current crisis? Assuming my late night calculations from the hotel room are correct, nominal GDP fell about 1.3% from 2008-2009. So how in the heck does that give us a ~10% unemployment rate? (You might ask, "What about the cumulative fall from 2007-2009?" But don't, because GDP in 2008 was higher than in 2007.)

Now maybe Scott would come back and refine the growth rates, and show that something happened in the 3rd quarter of 2008 that my annual figures above are smoothing out of existence. OK fine, but I don't think there's any way Scott is going to generate a recent fall in nominal GDP anywhere close the (almost) 17% one-year drop from 1920-1921. And yet, assuming the stats are measuring the same thing, the unemployment back then was just a point or two higher than it has been in our time.

Now let's move on to the decisive issue. Over email I asked Scott about these things, and he said (reproducing with permission), "Yes, there was a huge drop in NGDP in 1921, but I don't see where you are going with this. I agree with the Austrian view that a sharp fall in NGDP is a bad thing, and 1921 certainly supports that, as does 1929-33, when NGDP fell in half. I'm curious to hear your take on it."

So I said, "OK, I'm saying why did the economy escape a decade of depression in the 1920s--in fact had the Roaring 20s--when in the beginning, the 1920-1921 crash was worse (according to your theory) than the Great Depression crash? Did the Fed start targeting NGDP in 1921?"

Then Scott replied:

Bob, The 1921, 1930 and 1938 depressions were almost equally severe, as my theory predicts. The reason 1929-33 was far worse than 1920-21, is that NGDP fell in half between 1929 and 1933. Even by 1931, NGDP had fallen more steeply than in 1920-21. I think 1920-21 fits my theory perfectly, and make that argument in my book.(Hang on kids, we're almost to the finish line.) I came back with this gem: "But wait a second, of course if the economy recovers from a depression (whether because of wise Keynesian stimulus, Sumnerian Fed policy, or Austrian chanting) NGDP will recover. But I'm saying, can you point to what the Fed did to cause NGDP to recover in late 1922?"

And yes, Strong was basically targeting NGDP in the 1920s. He said he was concerned about fluctuations in both prices and real output; that's essentially NGDP targeting. NGDP grew fairly steadily between 1921-29, which is why the economy did well. When it fell in half after 1929, the economy did poorly. If NGDP had kept falling after 1921, as it did after 1930, the 1921 depression would have been much worse.

The 1921 depression was short, but deeper than our current recession. It ended quickly because NGDP recovered strongly in late 1922.

Scott explained: "The [monetary] Base fell sharply in 1921, and rose sharply in 1922."

OK for those who are still with me, let me show you how difficult it is to square the numbers on monetary base growth to fit Scott's narrative from above.

In the chart below, I have taken the St. Louis Fed's "Adjusted Monetary Base" series, the non-seasonally adjusted one. The data is monthly, which made it hard to see broad trends. So what I first did was construct quarterly averages out of the monthly data.

Then, I constructed 6-month growth rates for each quarter. So for example, the entry for 1920 1Q is 16.3%. What that means is that the average monetary base level in the 1st quarter of 1920 was 7.86% higher than the level in 3Q 1919. Since the base by 1st Q 1920 had grown 7.86% over the past 6 months, that works out to an annualized growth rate of monetary base of 16.3%. OK?

Now that you understand what the growth rates mean, check out this table:

I've put the significant money tightening periods in red, and the loosening periods in green. Now pretend for a minute that you knew nothing of the time periods, and you were applying Scott's theory. You want to predict which periods have the worst recessions.

OK the biggest reduction in monetary base occurs in 1921. It's true, the drop in 1937 is bad, but clearly the 1921 drop is worse. And the drop in 2008 is...oh wait, there was no drop in base. You just saw a slowdown in its growth.

Now at this point, we would expect the worst depression in US history to be in 1921, the second worst to be in 1937, and the third worst in 1930. We wouldn't even expect there to be a depression in 2008. (You can't see it in the excerpts I've given you, but there were other periods post-WW2 where monetary base actually fell or grew very anemically, and yet I don't think [off the top of my head] there were bad recessions in those periods. Clearly not "the worst Depression since WW2" which is what we are currently experiencing.)

OK let's be fair to Scott. He could argue that we need to look at the Fed's rescue of the economy in 1922, when (per Scott's email) monetary base grew rapidly. So we should expect to see the most phenomenal growth in monetary base in 1922, in order to counteract the huge restriction in the base in 1921. Otherwise, it would remain a mystery how the economy bounced back so quickly in 1922.

Uh oh. My measure of base growth was negative through the first half of 1922. And then even when it picked up, the highest it hit was 11.1% in the 4th quarter of 1922. Remember, unemployment had dropped about five percentage points--falling about in half--from 1921 to 1922.

So if the second-half spurt in 1922 explains the dramatic recovery--and indeed paved the way for the Roaring Twenties--then what was the problem in late 1931? The growth in monetary base then was much bigger than in late 1922. And yet we all know that unemployment continued to rise.

A similar puzzle occurs when we look at the huge, and consecutive, growth rates in 1938 and 1939. But unemployment was 19% in 1938, and was still 14.6% in 1940. Scott can give a story about "long and variable lags" to blame the spike in unemployment in 1938 on the monetary contraction in 1937, but how can he explain the post-1921 recovery by monetary base spurts that are pipsqueaks compared to the huge injections frmo 1938-1940?

Up till this point, Scott could maybe get by with a story that involved judicious use of cumulative effects etc. But look now to the green cells in late 2008 and early 2009. !!

I submit that Scott has fallen prey to a money illusion. Of course it can screw things up if our fractional reserve system allows a huge contraction in the money supply when other things are falling apart in the real economy. But just look at the 1920-1921 episode compared to 2008-2009. It is unreasonable to say the basic cause of our current malaise is that the Fed tightened up in 2008 and then didn't open the spigots enough after the crisis set in. The numbers aren't even in the right ZIP code for that explanation.

Back to you, Scott.

(NOTE: I am writing this from a hotel room. I reserve the right to change the numbers above in case I googled the wrong unemployment rate for a certain year, or screwed up the division for computing nominal GDP losses.)

Recreating the Crime Scene at Jekyll Island

If the international bankers are smart, they will have added a secret ingredient to the catered lunch on Saturday. A bunch of us rebels are at Jekyll Island, where the blueprints for the Federal Reserve were designed--and they definitely fell into the wrong hands, namely, the hands of the guys who wrote them.

The classic work on all this stuff is The Creature from Jekyll Island: A Second Look at the Federal Reserve . I heard that it was a kook book (not to be confused with a cook book) but I'm about halfway through and I'm waiting to hit the crazy stuff. Of course, it could just be that I'm crazy.

. I heard that it was a kook book (not to be confused with a cook book) but I'm about halfway through and I'm waiting to hit the crazy stuff. Of course, it could just be that I'm crazy.

The classic work on all this stuff is The Creature from Jekyll Island: A Second Look at the Federal Reserve

Tuesday, February 23, 2010

Zbigniew Brzezinski: How Jimmy Carter and I Started the Mujahadeen

If I didn't know any better, I'd say this was a conspiracy theory involving high-ranking US government officials, so it can't possibly be right... But anyway check out this amazing 1998 interview of Zbigniew Brzezinski that Brad DeLong dug up:

Interview of Zbigniew Brzezinski, Le Nouvel Observateur (France), Jan 15-21, 1998, p. 76*I am quite sure that if some "nutjob" posited this theory in 1980, he would be denounced as a paranoid pinko: "Yeah right, as if the US provoked the Soviet Union. Do you believe everything the Russkies tell you? I'm sure. Next you'll be telling me the Soviets felt threatened with all those nuclear warheads pointed at them. Like the US would ever nuke people. That's something Iranians would do, not us. We're the good guys."

Q: The former director of the CIA, Robert Gates, stated in his memoirs ["From the Shadows"], that American intelligence services began to aid the Mujahadeen in Afghanistan 6 months before the Soviet intervention. In this period you were the national security adviser to President Carter. You therefore played a role in this affair. Is that correct?

Brzezinski: Yes. According to the official version of history, CIA aid to the Mujahadeen began during 1980, that is to say, after the Soviet army invaded Afghanistan, 24 Dec 1979. But the reality, secretly guarded until now, is completely otherwise: Indeed, it was July 3, 1979 that President Carter signed the first directive for secret aid to the opponents of the pro-Soviet regime in Kabul. And that very day, I wrote a note to the president in which I explained to him that in my opinion this aid was going to induce a Soviet military intervention.

Q: Despite this risk, you were an advocate of this covert action. But perhaps you yourself desired this Soviet entry into war and looked to provoke it?

Brzezinski: It isn't quite that. We didn't push the Russians to intervene, but we knowingly increased the probability that they would.

Q: When the Soviets justified their intervention by asserting that they intended to fight against a secret involvement of the United States in Afghanistan, people didn't believe them. However, there was a basis of truth. You don't regret anything today?

Brzezinski: Regret what? That secret operation was an excellent idea. It had the effect of drawing the Russians into the Afghan trap and you want me to regret it? The day that the Soviets officially crossed the border, I wrote to President Carter: We now have the opportunity of giving to the USSR its Vietnam war. Indeed, for almost 10 years, Moscow had to carry on a war unsupportable by the government, a conflict that brought about the demoralization and finally the breakup of the Soviet empire.

Q: And neither do you regret having supported the Islamic [integrisme], having given arms and advice to future terrorists?

Brzezinski: What is most important to the history of the world? The Taliban or the collapse of the Soviet empire? Some stirred-up Moslems or the liberation of Central Europe and the end of the cold war?

Q: Some stirred-up Moslems? But it has been said and repeated: Islamic fundamentalism represents a world menace today.

Brzezinski: Nonsense! It is said that the West had a global policy in regard to Islam. That is stupid. There isn't a global Islam. Look at Islam in a rational manner and without demagoguery or emotion. It is the leading religion of the world with 1.5 billion followers. But what is there in common among Saudi Arabian fundamentalism, moderate Morocco, Pakistan militarism, Egyptian pro-Western or Central Asian secularism? Nothing more than what unites the Christian countries.

* There are at least two editions of this magazine; with the perhaps sole exception of the Library of Congress, the version sent to the United States is shorter than the French version, and the Brzezinski interview was not included in the shorter version.

Can I Pass the Keynesian Turing Test?

Robert Barro has a pretty interesting WSJ op ed today, in which he uses his historical analysis of government spending and tax multipliers to evaluate the Obama Administration's stimulus package of 2009.

In a nutshell, Barro first estimates a spending multiplier of 0.4 (in the first year) and a tax multiplier of -1.1. So if the government spends $100 billion and doesn't touch taxes (i.e. borrows and spends an extra $100 billion), then GDP goes up by $40 billion. What that means is that there is 60% crowding out. The expenditure of $100 billion directly raises GDP by $100 billion, but then other components of GDP (private consumption, investment) fall by $60 billion. Hence, the net effect on GDP (in the first year) from an additional $100 billion in deficit-financed spending is only$60 $40 billion, according to Barro's analysis of periods of big spurts in military spending.

On the other hand, Barro finds that if the government raises $100 billion in new taxes (while holding spending constant), this lowers GDP by $110 billion.

So putting the two effects together, Barro estimates the 5-year impact of the stimulus plan. The idea is that the government "buys" some output on the front end (because the spending multiplier is above 0), but then has to forfeit output (relative to the baseline) on the back end because the higher debt requires more taxes. Barro concludes:

In a nutshell, Barro first estimates a spending multiplier of 0.4 (in the first year) and a tax multiplier of -1.1. So if the government spends $100 billion and doesn't touch taxes (i.e. borrows and spends an extra $100 billion), then GDP goes up by $40 billion. What that means is that there is 60% crowding out. The expenditure of $100 billion directly raises GDP by $100 billion, but then other components of GDP (private consumption, investment) fall by $60 billion. Hence, the net effect on GDP (in the first year) from an additional $100 billion in deficit-financed spending is only

On the other hand, Barro finds that if the government raises $100 billion in new taxes (while holding spending constant), this lowers GDP by $110 billion.

So putting the two effects together, Barro estimates the 5-year impact of the stimulus plan. The idea is that the government "buys" some output on the front end (because the spending multiplier is above 0), but then has to forfeit output (relative to the baseline) on the back end because the higher debt requires more taxes. Barro concludes:

We can now put the elements together to form a "five-year plan" from 2009 to 2013. The path of incremental government outlays over the five years in billions of dollars is +300, +300, 0, 0, 0, which adds up to +600. The path for GDP is +120, +180, +60, minus 330, minus 330, adding up to minus 300. GDP falls overall because the famous "balanced-budget multiplier"—the response of GDP when government spending and taxes rise together—is negative. This result accords with the familiar pattern whereby countries with larger public sectors tend to grow slower over the long term.OK I wanted to test whether I really understand the Keynesian mindset. So I honestly haven't looked yet to see what DeLong and Krugman have to say about this. Here's my guess:

The projected effect on other parts of GDP (consumer expenditure, private investment, net exports) is minus 180, minus 120, +60, minus 330, minus 330, which adds up to minus 900. Thus, viewed over five years, the fiscal stimulus package is a way to get an extra $600 billion of public spending at the cost of $900 billion in private expenditure. This is a bad deal.

The fiscal stimulus package of 2009 was a mistake. It follows that an additional stimulus package in 2010 would be another mistake.

My Guesses as to the Keynesian Response to Barro's Op EdOK kids, go look. I promise this was off the top of my head. How did I do?

(1) Barro is a liar, second only to Russ Roberts in his lyinghood.

(2) Barro's spending multiplier is way too low. He admits that he derives it from studying wartime periods, but that's absurd. During such periods, the government enacts strict rationing measures to ensure that private consumption and investment stay suppressed, freeing up resources for the war effort.

(3) Barro's use of the 2008 baseline is absurd. If the government had sat back and done nothing, unemployment would have continued climbing, perhaps it would have been 15% right now. That would mean lower tax revenues and more spending on social welfare programs. In essence, all the stimulus does is concentrate that unavoidable government debt increase into the beginning years, when it might obviate much of the later spending. Barro has done the equivalent of looking at a patient just diagnosed with cancer, and comparing the medical expenses of early intervention against a "baseline" of a perfectly health person's medical costs.

(4) Barro's spending multiplier makes no sense, both in theory and in terms of empirical evidence. In an economy with 10% unemployment and 0% interest rates, running a fiscal deficit doesn't cause any crowding out. We would see the telltale signs if it did. So right now, when the government spends an extra $100 billion with borrowed money, that doesn't cause a $60 billion reduction in spending elsewhere. How could it? What is the mechanism? And not only does the $100 billion raise GDP directly by that amount, with no $60 billion offset, but in fact we get further GDP gains because of the further spending by people who would otherwise have been unemployed. Barro casts aspersions on Christina Romer's estimates of a multiplier greater than 1, but he doesn't explain what her mistake was. He just says he can't understand her figures and asserts his own. What pseudoscientific nonsense. Why oh why can't we get right wing economists who know more than discredited views from the 1930s?

Monday, February 22, 2010

Taylor Conant Asks: Do We Live in a Movie?

Here's the rest of his email:

A bad one? Just saw this ad:

So, here's the script-- a government take-over of a major auto manufacturer, who happens to be dabbling in onboard vehicle "safety" technology that allows the company's vehicles to be controlled from a central location, and the competition is being brought down by legislative and executive agency inquiries and hearings, and a police force that is increasing militarized and has been indoctrinated to see civilians as game to be hunted and dominated. A psychological thriller exploring the psychosis of the hunters and the fearful desperation of the hunted as they try to escape the fast-enclosing walls of a terrifying police state. oh, and they're being RFIDed, too.

Submitizen, coming December 2010, tag line "Nowhere to run, nowhere to hide."

I mean seriously, any idiot should be able to see "Hmm, if the cops can get my stolen vehicle back that easily, I also can be easily detained, say if they suspect me of drunk driving, running drugs, etc. and then proceed to be harassed" but of course, they won't.

Two Cheers for Credit Cards

(Not three cheers, mind you.) The intro:

Ever since someone in grad school deviously introduced me to the concept of "irrational" debt aversion, I have been carrying credit-card balances that are far too high. Believe me, I understand the tricks these companies pull, like the clause in fine print where you unwittingly pledged away your firstborn.And if you want to see what's good about credit cards, you'll have to read the article.

I have had credit-card employees explain matter-of-factly to me that it was in my interest that they apply payments to the balances with the lowest interest rates first, and I was once driven to vulgarity on the phone by a representative who got philosophical with me when I was trying to close an account with a zero balance.[1] So believe me when I say that I get it when people complain about credit-card companies.

Yet in the present article I want to describe some of the benefits of these seductive tools of a modern financial economy. Although many critics would argue that credit cards show the flaws of capitalism, they also showcase its strengths.

More Disinflation Disinformation

In a recent blog post titled, "More on Disinflation" Paul Krugman comments on the headlines trying to interpret the recent CPI announcement:

Also of relevance is the fact that Krugman focused on an odd time frame. Here's the full picture:

Now is it really jumping out at you that the Price Index of Personal Consumption Expenditures--stripped of food and energy--go down during recessions?

And even in the periods where it does seem to work, is the mechanism really the Keynesian one about recessions being caused by a fall in aggregate demand? Couldn't you just as easily explain it by saying that people have to buy food and energy, and so when their prices spike--especially if it's during tough times--then the prices of everything else tend to fall?

In other words, my point here is that people say, "Oh we're stripping out volatile food and energy to look at the underlying trend." But since people care a lot more about food and energy than a lot of the remaining purchases, that's closer to throwing out the trend and looking at the residual.

As Mark Thoma recently suggested...it’s odd that most macroeconomic forecasts show inflation remaining stable or even rising despite continuing very high unemployment. Both history and logic suggests that this is wrong.If you want to see me tackle the claim that both theory and history support Krugman's belief that high unemployment ==> low price inflation, see my recent Washington Times op ed.

And declining inflation is clear using any core measure. The Fed, I happen to know, tends to focus on the core personal consumption expenditure deflator:

There are some strange bobbles in this measure, suggesting that it’s not as good a measure of inertial inflation as advertised, but leaving that aside we see, once again, serious disinflation as a result of the recession.

I still think there’s a real risk we’ll turn Japanese.

{kind=link}

{kind=link}

Also of relevance is the fact that Krugman focused on an odd time frame. Here's the full picture:

Now is it really jumping out at you that the Price Index of Personal Consumption Expenditures--stripped of food and energy--go down during recessions?

And even in the periods where it does seem to work, is the mechanism really the Keynesian one about recessions being caused by a fall in aggregate demand? Couldn't you just as easily explain it by saying that people have to buy food and energy, and so when their prices spike--especially if it's during tough times--then the prices of everything else tend to fall?

In other words, my point here is that people say, "Oh we're stripping out volatile food and energy to look at the underlying trend." But since people care a lot more about food and energy than a lot of the remaining purchases, that's closer to throwing out the trend and looking at the residual.

Sunday, February 21, 2010

Economics, Selfishness, and the Gospel

The comments on my first attempt got swamped. (Hey kids, can we please drop the potty talk?)

The problem is that people started arguing about something that was irrelevant--I could say "orthogonal" to impress you--to my criticism of Bryan Caplan. So let me state it again. Maybe I'm wrong, but none of the critics (in particular Gene Callahan) in the comments of my original post addressed the crucial issue.

There are at least three similar questions revolving around this discussion:

(1) Is there a useful distinction between selfish and altruistic actions? Yes I think there is. Bryan and Gene agree with me.